|

| Ingin Bayar Listrik Hemat? Coba Tekan Kode Rahasia di Meteran Anda |

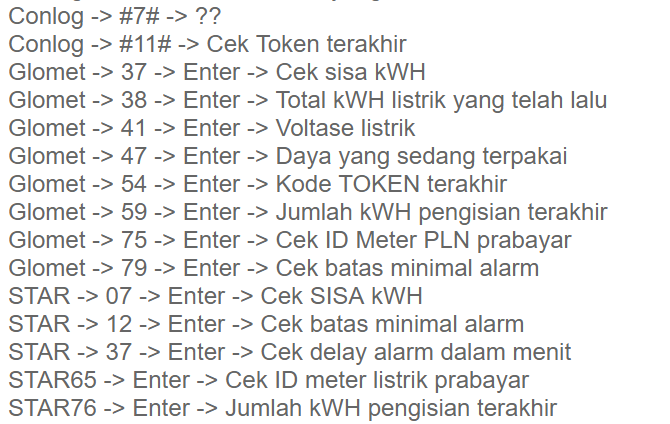

Ingin Bayar Listrik Hemat? Coba Tekan Kode Rahasia Berikut di Meteran Anda

Life Insurance - Learn From an Old Agent

Life Insurance is an insurance product that pays at the death of the insured. It really should be called "Death Insurance," but people don't like that name. But it insures the death of an individual. Actually, what is insured is the economic loss that would occur at the death of the person insured.

Those economic losses take a lot of different forms, such as:

- the income stream of either "breadwinner" in a family

- the loss of services to the family of a stay-at-home-mom

- the final expenses at the death of a child

- final expenses of an individual after an illness and medical treatment

- "Keyman" coverage, which insures the owner or valuable employee of a business against the economic loss the business would suffer at their death

- estate planning insurance, where a person is insured to pay estate taxes at death

- "Buy and Sell Agreements," in which life insurance is purchased to fund a business transaction at the untimely death of parties in the transaction

- Accidental death insurance, in which a person buys a policy that pays in case they die due to an accident

- Mortgage life insurance, in which the borrower buys a policy that pays off the mortgage at death - and many more.

Life insurance has been around for hundreds of years, and in some cases, has become a much better product. The insurance companies have been able to develop mortality tables, which are studies of statistical patterns of human death over time...usually over a lifetime of 100 years. These mortality tables are surprisingly accurate, and allow the insurance companies to closely predict how many people of any given age will die each year. From these tables and other information, the insurance companies derive the cost of the insurance policy.

The cost is customarily expressed in an annual cost per thousand of coverage. For example, if you wanted to buy $10,000 of coverage, and the cost per thousand was $10.00, your annual premium would be $100.00.

Modern medicine and better nutrition has increased the life expectancy of most people. Increased life expectancy has facilitated a sharp decrease in life insurance premiums. In many cases, the cost of insurance is only pennies per thousand.

There is really only one type of life insurance, and that is Term Insurance. That means that a person is insured for a certain period of time, or a term. All of the other life insurance products have term insurance as their main ingredient. There is no other ingredient they can use. However, the insurance companies have invented many, many other life products that tend to obscure the reasons for life insurance. They also vastly enrich the insurance companies.

Term Insurance

The most basic life insurance is an annual renewable term policy. Each year, the premium is a little higher as a person ages. The insurance companies designed a level premium policy, which stopped the annual premium increases for policyholders. The insurers basically added up all the premiums from age 0 to age 100 and then divided by 100. That means that in the early years of the policy, the policyholder pays in more money that it takes to fund the pure insurance cost, and then in later years the premium is less than the pure insurance cost.

The same level term product can be designed for terms of any length, like 5, 10, 20, 25 or 30 year terms. The method of premium averaging is much the same in each case.

But this new product caused some problems. Insurers know that the vast majority of policyholders do not keep a policy for life. Consequently the level term policyholders were paying future premiums and then cancelling their policies. The insurance companies were delighted because they got to keep the money. But over time, they developed the concept of Cash Value.

Cash Value Insurance

With Cash Value insurance, a portion of the unused premium you spend is credited to an account tied to your policy. The money is not yours...it belongs entirely to the insurance company. If you cancel your policy and request a refund, they will refund that money to you. Otherwise, you have other choices:

1. Use the cash value to buy more insurance

2. Use the cash value to pay existing premiums

3. You may borrow the money at interest

4. If you die, the insurance company keeps the cash value and only pays the face amount of the insurance policy.

So, does this cash value product make sense? My response is "NO!"

Cash Value Life Insurance comes in lots of other names, such as:

- Whole Life

- Universal Life

- Variable Life

- Interest Sensitive Life

- Non-Participating Life (no dividends)

- Participating Life (pays dividends)

Many life insurance agents and companies tout their products as an investment product. But cash value insurance is not an investment. Investment dollars and insurance premiums should never be combined into one product. And investment dollars should NEVER be invested with an insurance company. They are middle men. They will take your investment and invest it themselves, and keep the difference.

Think about the methods that agents use to sell life insurance, and compare them to any other type of insurance. What you'll see is that life insurance sales tactics and techniques are ridiculous when compared to other insurance products.

Would you ever consider buying a car insurance policy, or homeowners policy, or business insurance policy in which you paid extra premium that the insurance company kept, or made you borrow from them? But, curiously, life insurance agents have been wildly successful convincing otherwise intelligent people that cash value life insurance is a good product to buy.

Care to guess why insurance agents have aggressively sold cash value insurance and eschewed term insurance?

Commissions.

The insurance companies have become vastly wealthy on cash value insurance. So, to encourage sales, they pay huge commissions. Term insurance commissions can range from 10% to 50%, sometimes even 100%. But cash value insurance commissions can be up to 100% of the first year's premium, and handsome renewal commissions for years after.

But it's not just the commission rate that matters. It's also the premium rates that come into play. Term insurance is FAR CHEAPER than cash value insurance.

Here's an example of a 30 year old male, non-smoker, buying $100,000 of coverage:

Term insurance costs $0.50 per thousand for a premium of $50.00. At 100% commission, the commission would be $50.00.

Cash Value insurance costs $12.50 per thousand for a premium of $1,250.00. At 100% commission, the commission would be $1,250.00.

So you see that it would be easy for an agent to place his own financial well-being ahead of the well-being of his client. He would have to sell 25 term policies to make the same commission as only one cash value policy.

But, in my opinion, that agent would have violated his fiduciary duty to the client, which is the duty to place the client's needs above his own. The agent would also have to set aside his conscience.

My opinion is that life insurance agents operate from one of three positions:

1. Ignorance - they simply don't know how cash value insurance works.

2. Greed - they know exactly how cash value insurance works and sell it anyway.

3. Knowledge and Duty - they sell term insurance.

Which agent do you want to do business with?

How do I know this stuff? Because I sold cash value life insurance early in my career.

When I started as an insurance agent in 1973 I knew absolutely nothing about how life insurance worked. The insurance company taught me to sell whole life insurance, and to discourage clients from term insurance. But, after some time of reading and research, I learned that cash value insurance is a bad deal. I began to sell only term insurance. I refused to set aside my conscience. I also went back to some early clients and switched their policies from cash value to term.

The insurance company fired me for that decision.

I found a new insurance company that only sold term insurance and also paid high commissions. I made a good living selling term insurance, so I know it can be done.

So, as you shop for life insurance, please accept the advice of an old agent. Never, never, ever buy cash value life insurance. Buy term insurance.

Now, I'd like to offer you two special reports at no cost. One is "5 Things To Do When Shopping For Car Insurance," and the other is "5 Things To Avoid When Shopping For Car Insurance." Each one is a $9.95 value, but free to you when you sign up for my newsletter at the website address below.

Article Source: http://EzineArticles.com/2661313